Experiment: The Reality of My Starting Point

Everything up to this point has been about Theory — stepping back from tactics and focusing on clarity first. But this journal wouldn’t be much of an experimental application to reality if I didn’t practice what I preached.

What follows isn’t a template or a set of rules. It’s showing you what this looks like in real life - where I am now, and how I’m applying these ideas to my own situation, and with full awareness that this will change over time.

What you are about to read is real. It isn’t a flex, and it isn’t polished. These numbers aren’t impressive – but they’re honest.

Finding My Why

I never wanted a traditional working life – not at 18 years old, not now either. I value time and freedom over status and titles. So, like many, I did what was sensible at the time I started saving. Saving without fully having a clear goal or timeline in place. This abstract goal lead to me saving inconsistently, saving well some months, and spending like I had all the money in the world another month.

This blurry, unclear goal would be my downfall if I did not change something. I needed a purpose…

Why do I want to achieve Financial Independence, and “retire”?

I want to be able to choose when and how to work.

I want to free up some time to spend with family, friends, and on hobbies/passions that give me hoy.

I want to travel, relax, and make the odd purchase where I don’t have to worry about what I will need to sacrifice later to have to pay for this now.

Set my Goal

Using a typical goal setting guide, I built it SMART:

S-pecific: I want to save enough so that by the time I retire, my investments can cover my living costs.

M-easurable: Tracking my net-worth through a portfolio, active income, and passive income.

A-chievable: (Defined a flexible savings rate that can be adjusted). Save and invest 50+% of my income and re-adjust when new life factors are added.

R-elevant: This goal supports my desire to work less when it matters, travel without guilt, and reduce financial stress over time.

T-timeframe: By age 50, I aim to reach financial independence where my portfolio covers my living costs.

Along the way, I (and you) will most likely develop many sub-goals to support the main goal. One such sub-goal of mine is to reach partial financial independence by age 43 to have the choice to work less should I desire.

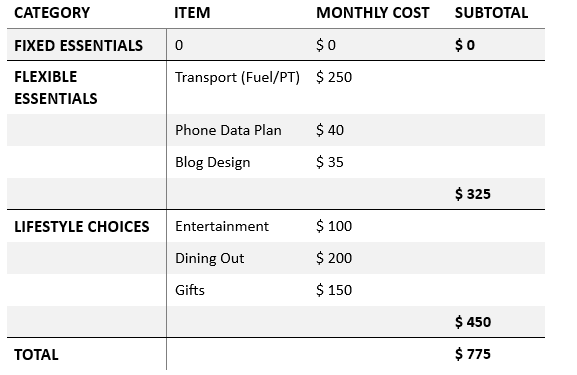

Find My Baseline

My current, not my ideal life cost.

This is where personal factors come heavily into play and determine how much your base saving rate can be before you begin optimizing. I am lucky enough to still live with my parents, and as such, my living costs are incredibly low. Everyone’s personal situations are different, and as such everyone’s baseline will be slightly, or fully, different.

With an income of around $50,000 to $60,000 NZD, this allows me to save around 70% of my post-tax income.

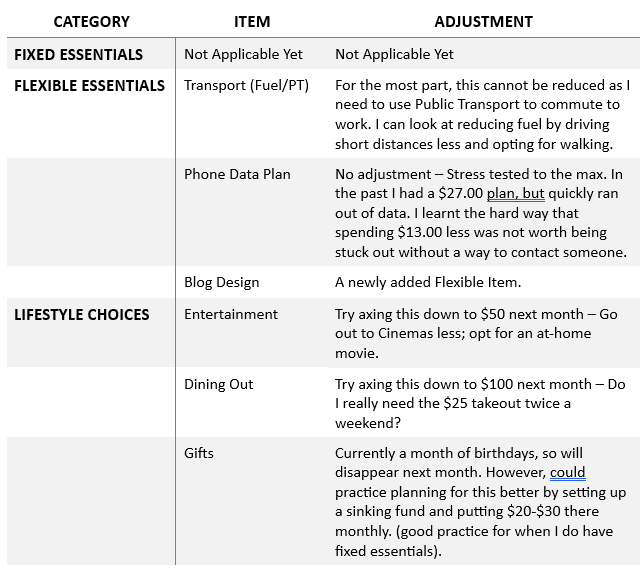

Stress-Testing my Baseline

For the most part, my baseline has been stress-tested. Since I do not have Fixed essentials, it has been easy to adjust – I know this won’t be the truth for everyone out there.

I know it may seem pointless trying to cut costs as I already save a fair amount due to the absence of fixed essentials, however it is good practice to get into the habit of stress-testing spending to achieve a goal so that when Fixed essentials do come in-to the equation, I am not left struggling to cut costs to save.

My FIRE Path

Incorporating all my personal factors – my purpose, my goals, and my baseline I chose a FIRE strategy that fits my lifestyle. Knowing that I want to retire with more spending choice than the basic necessities, I know Lean FIRE is not an option for me. I also know that due to future life events, I will not be able to save as aggressively down the line.

This may be as soon as 2 years from now, or as late as 10 years from now.

Knowing this, I have taken a mix of Barista, Coast, and Fat FIRE approach to my journey.

The main goal is to save as heavily as I can now, using time as my greatest ally to grow my investments (Coast FIRE) to a point where I can choose to reduce my hours or take on part-time work to cover basic living expenses (Barista FIRE), withdrawing minimal amounts so that my Portfolio still enjoys some compounding until I am ready enough to retire and live out a luxurious retirement (Fat FIRE).

This is the reality of my starting point.

It’s not meant to be perfect – but it is clear enough to move forward with intention.

From here, the focus shifts to consistency – building good habits, saving and investing steadily, and letting time do its work while life unfolds around it.

Progress will always be more powerful than perfection.

If you’re comfortable sharing, I’d be curious to hear what your starting point looks like — or what part of this journey you’re currently figuring out.