Taking Your First Steps

The context is set and you’re ready to start.

So how exactly do you start?

Most financial independence advice skips ahead to extreme frugality, investing, or income hacks. These are all crucial topics, but I learned the hard way that starting there felt like trying to run a marathon before I’d learned to walk.

When I first started down this path, I jumped between blogs, spreadsheets, and strategies without any clear direction.

I tried to save aggressively without knowing how much I could realistically save.

I wondered why I couldn’t hit the same savings rates these “Gurus” talked about and assumed I was doing something wrong.

It turns out I was doing something wrong – just not where I expected.

I didn’t know what I was saving for. Without a clear purpose, saving felt abstract – and that made it easy to undo.

I’d justify spending I didn’t need and treat money as something to be enjoyed now because the future goal felt vague.

Before I could run the marathon, I needed to learn how to crawl…

I found that the crucial step most advice skips is Clarity: understanding what you actually want before optimizing your lifestyle to get there.

Before trying to maximize savings rates or chase returns, you need to understand the life you’re trying to fund.

Without that clarity, it’s easy to move quickly in the wrong direction, traveling blindly down a road that is easy to get lost on without a map.

Find Your Why

Forget numbers for now. Start with purpose.

Why do you want financial independence? Is it to reduce stress? Take back your time? Create space for family, adventures, or just breathing easy?

For me, it’s a bit of everything. To live life on my own terms – without subconscious cash anxiety. I want the freedom to travel without guilt, to work less when it matters, and to spend time on the things that make my life feel full – family, friends, and experiences.

This “why” has become my anchor. It’s what stopped me from getting lost again. It’s what turned Financial Independence from a spreadsheet exercise into something real — something worth building toward.

Get Your Baseline

This isn’t a budget. It’s not a FIRE number and it’s definitely not about cutting things out – yet.

Your baseline is the cost of your current life. Not your ideal life.

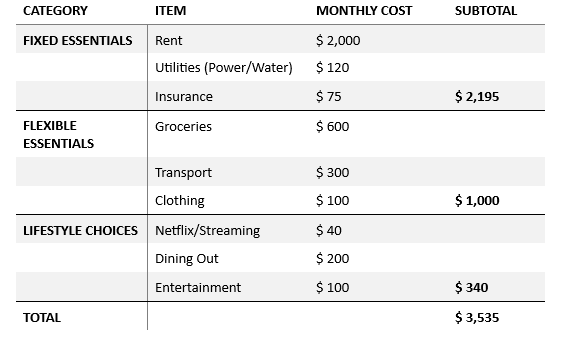

To find it, start by grouping your spending into three broad categories:

Fixed Essentials: Non-negotiables that don’t really move month-to-month. Rent/Mortgage, Utility bills, insurance.

Flexible Essentials: Must-haves with some wiggle room – groceries, transport, and basics

Lifestyle choices: The optional stuff - Subscriptions, entertainment, dining out.

Simple Example:

Stress-Test for “Enough”

Now begin to layer in your “why”. Question each category through that lens:

Fixed essentials: Can these shrink without pain? (switching power plans, changing insurance plans, scout cheaper rentals nearby)

Flexible Essentials: What’s the lean version that doesn’t sacrifice your quality of life? (Premium supermarkets vs discount supermarkets, bike/walk short trips over driving.)

Lifestyle choice: Joy vs habits. Keep Netflix if it recharges you; ditch cinema runs or $20 impulse takeaways.

Pick your FIRE

Many blogs about FIRE will tell you there’s only one path to FIRE – extreme frugality. Slash everything, live on the bare minimum. But FIRE has more paths, and the best one is the one that adapts to your lifestyle rather than fighting it.

Lean FIRE: The ‘traditional’ path bloggers seem to take: For those who have lower-than-average expenses and can live off a lot less money than others now, and plan to in the future. By focusing on aggressive savings and frugal living, you can reach your goal faster.

This is ideal for those who value time over luxury, as you likely won’t have much room for spending beyond necessities.Coast FIRE: A long-term approach that utilizes time and compounding as an ally.

By saving heavily in your early career you allow your investments to grow on their own to cover retirement. You can then slowly reduce/stop contributing if required. Ideal for those starting younger, planning for future lifestyle creep or family, and wanting flexibility later in life.Fat FIRE: Opposite of Lean FIRE with similar principles. For those who wish to maintain (or upgrade) to a high-end lifestyle. It still requires aggressive savings and investing, but you will be aiming for a higher portfolio value than Lean FIRE so you don’t have to limit spending as much. Ideal for high-income professionals, dual income couples, or simply those who wish to live a lavish lifestyle in retirement.

Barista FIRE: Hate the soul-crushing 9-5? This strategy allows individuals to leave high-stress, full-time jobs earlier than traditional retirement age, while taking on part-time gigs to cover the income gap. Like Coast, you save a lot early on, but choose to leave full-time work earlier, allowing part-time work (like Barista) to cover basic costs while making small withdrawals to ‘top-up’ your lifestyle. Ideal for burnt-out workers craving time now, and those who wish to keep busy in retirement.

Truth is, there are many different ways to achieve this goal, and what works for you may not work for another. Perhaps you can live lean, perhaps you want luxury, or maybe you blend part-time work with luxury extras.

There’s no single path to FIRE, but every path starts the same way: Clarity.

Track your baseline. Lock in your why. Choose a path that fits.

What's your why?

Share below.