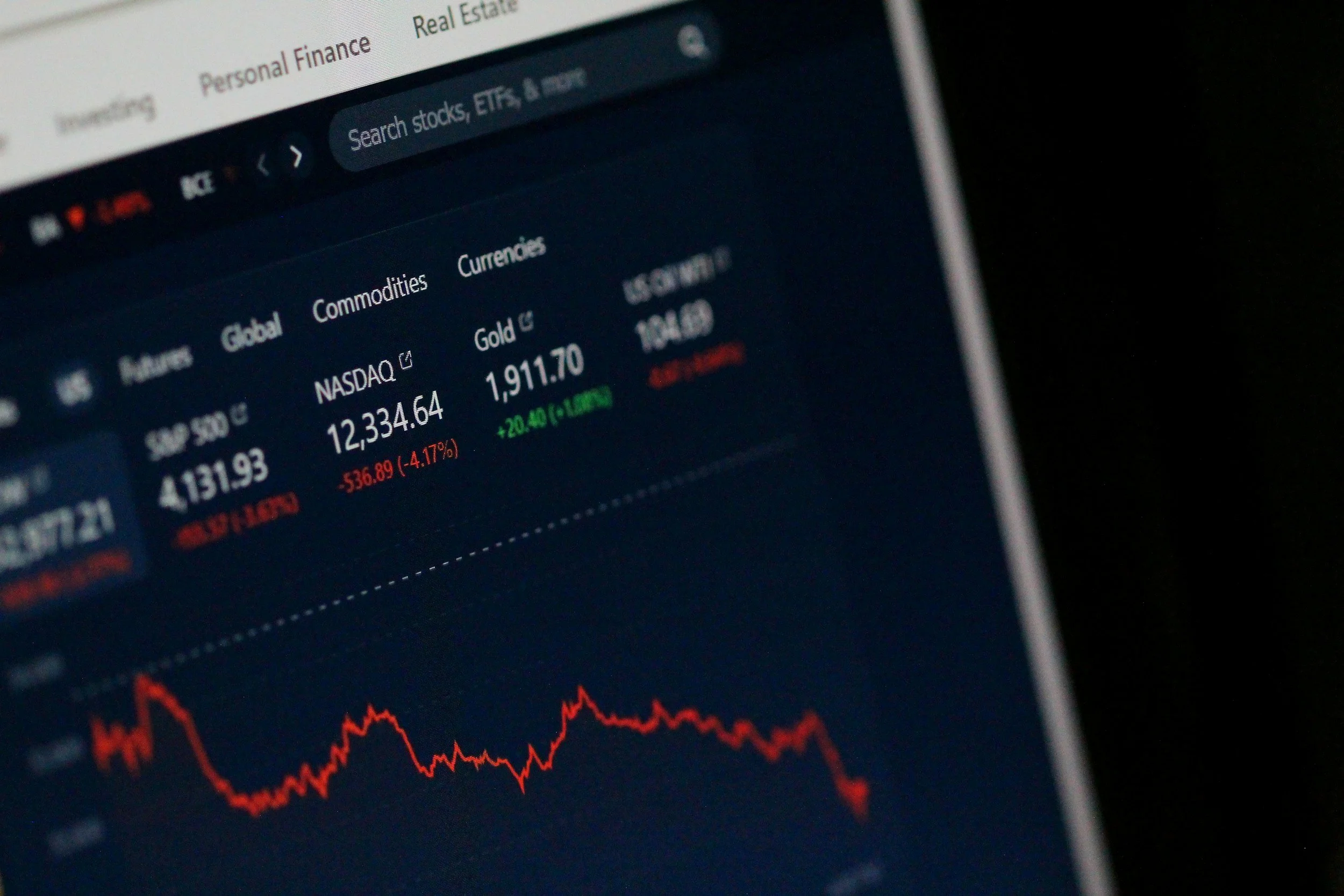

FIRE Under Fire: Staying the Course When the World’s on Fire

War has a way of making long-term plans feel suddenly fragile. One day you're on the path — saving, investing, building quietly toward Financial Independence — and the next, the world is on fire and your portfolio is caught in the blast radius.

The US-Israeli conflict with Iran has sent shockwaves through global energy markets, reignited inflation fears, and left even the most disciplined investors quietly questioning everything. Should you keep investing? Hold cash? Wait it out?

This post won't tell you what you want to hear. It'll tell you what history actually shows — about markets, about crises, and about the investors who come out the other side stronger than when they went in.

Simple Steps to Smarter Budgeting

Here is a common scene:

Someone earning a decent salary feels like they’re always “Just getting by,” yet can’t quite explain where the money goes each pay cycle.

What makes this especially frustrating is that most people don’t actually track their spending. They estimate it. And those estimates are usually way off — often by 20–30%. That gap between what we think we spend and what we actually spend is where financial stress lives.

For some reason, budgeting has become something people quietly avoid admitting they need, carrying a stigma similar to dieting, being seen as restrictive or a sign that you’re broke.

But, budgeting isn’t about restriction. It isn’t about saying no to everything you enjoy, living on rice and beans, or tracking every dollar until the fun disappears from your life instead of your money.

And it’s definitely not a punishment for being bad with money.

A budget is simply deciding where your money goes before it disappears.

Experiment: The Reality of My Starting Point

Everything up to this point has been about Theory — stepping back from tactics and focusing on clarity first. But this journal wouldn’t be much of an experimental application to reality if I didn’t practice what I preached.

What follows isn’t a template or a set of rules. It’s showing you what this looks like in real life - where I am now, and how I’m applying these ideas to my own situation, and with full awareness that this will change over time.

What you are about to read is real. It isn’t a flex, and it isn’t polished. These numbers aren’t impressive – but they’re honest…

Taking Your First Steps

Most Financial Independence Advice jumps straight into investing and debt reduction, but misses a crucial step.

Before starting your Journey to Financial Independence, you need clarity - a goal.

Without this it is easy to get lost along the road to Financial Independence.

What’s your why? Why are you wanting to achieve Financial Independence?

What’s your baseline? Your current cost of life?

Test this - can it be cut?

Choose your FIRE. The different types of FIRE and who they are best suited for.

Once you know this, you can optimize your life to suit.

What the Postcard Version of New Zealand doesn’t say…

Snow-capped mountains, endless coastlines, and cafés buzzing on a Friday morning make it easy to believe New Zealand has cracked the code to a good life. I thought so too when I first arrived six years ago. But behind the postcard moments sits a very different reality — early alarms, rising rents and mortgages, and a quiet anxiety about the cost of living

This contrast shapes every conversation about Financial Independence in modern-day New Zealand. When cost of living rises faster than incomes, the foundation FIRE relies on begins to shrink.

That doesn’t mean FIRE is dead — it means it has to adapt. In New Zealand, that often looks like longer timelines, lower targets, and lifestyle-first design rather than rigid formulas…

America vs New Zealand: Breaking Down the Numbers

American FIRE advice looks great on paper, until you try applying it in New Zealand.

By briefly breaking down income, cost of living, geography, and tax systems, this article shows why U.S.-centric FIRE strategies don’t translate cleanly to a Kiwi (or global) lifestyle — and why FIRE needs recalibration outside America.

Why Most FIRE Advice Doesn’t Work in New Zealand (And What I am Doing About it)

Most FIRE advice assumes you live in America. I don’t. At 23, I’m not an expert—but I am curious, intentional, and tired of advice that ignores local reality. This is the start of my journey toward financial independence in New Zealand, and documents what happens when you stop copying the US playbook and start building your own.